Mox is the winner. Unlike other blogs with referral links for all cards, only if you read my post, agree with my opinion, and manually paste in my Mox referral code of TJGQ47 do I make any money.

Standard Chartered or Mox?

If you're new to credit cards and are in the process of applying for your first card, learn that it is a 2-way street. Sometimes you pick the card and sometimes the bank picks you. Your choice of card depends first on whether you meet the bank's requirements for issuing the card.

| Bank | Card Type | Foreign Transaction Fee | Min. Income Requirement |

|---|---|---|---|

| Standard Chartered | Visa | 1.95% | $96K |

| Mox | Mastercard | 1.95% | None |

Mox is the overall winner here IMHO as I am supportive of financial inclusion. The absence of a listed Minimum Income Requirement makes Mox the better choice over Standard Chartered which has a $96K annual income requirement.

Mox has no minimum income requirement

If you travel and/or make overseas purchases (including online), the identical Foreign Transaction Fees between Visa and Mastercard do not make it much easier for you to decide, but what if I told you Mox is better because:

Mastercard generally offers better foreign exchange rates than Visa

So there you have it. 2 points to Mox, zero points to Standard Chartered.

Cashback or Miles card?

Open a Mox bank account with $600K to solve this dilemma

You can switch between cashback and miles with Mox.

- Free if you have over $600K with Mox bank

- $50/switch if less than $600K with Mox bank.

This is 3 points for Mox and zero points to Standard Chartered.

Cashback

If you're still not convinced, let's dive deeper.

There are 3 cashback cards from Standard Chartered, all Visa Signature with a minimum income requirement of $96K. Strictly speaking it's 2 cashback cards and 1 points card (A. Point) with points redeemable for cash credit on your statement. There are 2 additional Mox cards via Standard Chartered's stake in Mox.

How to pick a cashback card

The table below lists all the cashback cards from Standard Chartered and Mox at a high-level.

| Card Name | Annual Fee | Foreign Transaction Fee | Cashback (Key Categories) | Cashback cap |

|---|---|---|---|---|

| Simply Cash Visa | $2K (1st yr waived) | 1.95% | 1.5% (Local Spend) 2% (Foreign Spend) |

Unlimited |

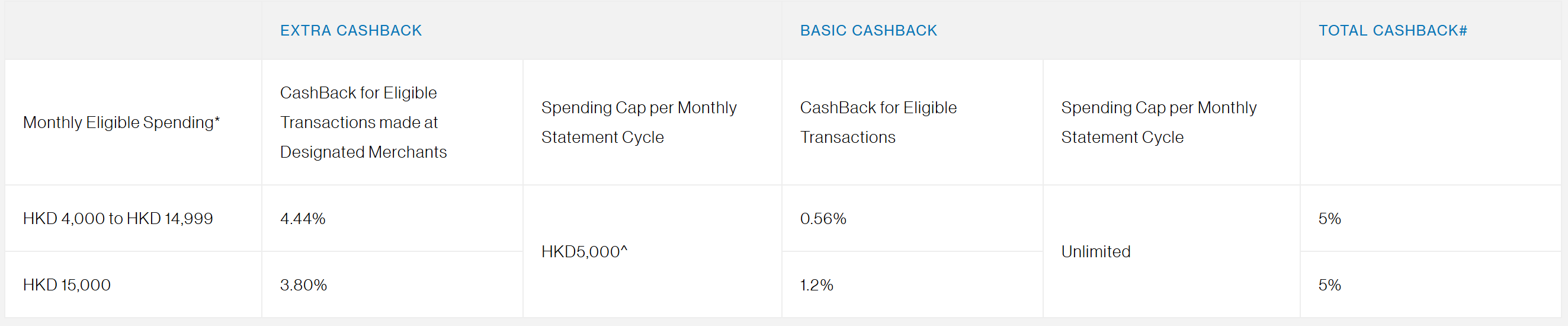

| Smart Card | Permanently Waived | 0% (Permanently Waived) | 5% (Designated merchants) 1.2% (Overseas) 0.56% (General) |

$250/month |

| A. Point Card | Permanently Waived | 1.95% | 0.05% (Foreign Spend) 1% (Bill Credit) 2% (redeeming select merchant coupons) |

$500/month |

| Mox+ | Waived | 1.95% | 2% (General) 3% (Groceries) |

Unlimited |

| Mox | Waived | 1.95% | 1% (General) 2% (with $25K/month payroll) 3% (Groceries) |

Unlimited |

While the one-off Welcome Offers for each card may play a factor in your decision making, I encourage you to consider the longer term impact, regardless of whether you spend money or not. Most Welcome Offers do have a spend requirement, so unless you were planning on spending, it may not be the best financial advice to spend just to get the Welcome Offer.

Here are some thoughts on how to go through the process of elimination to pick the right card to save money. Look for:

- No annual fee - this eliminates the Simply Cash Visa. By paying a fee upfront, you're already making it harder to get more back in return. Cards have fees because the bank exists to make money, and they want to encourage you to spend to get your money's worth. Every dollar you don't spend can be invested for potentially greater returns, so maximizing spending is a non-goal. Maximizing saving or benefits in return should be your goal. Permanently waived annual fee is because it is a key feature of the card, as opposed to waived, which means waived for now. Mox adjusts their terms and conditions or rewards on a quarterly basis. What is true now may not be the same 3 months from now.

- Cashback cap - this eliminates the Smart Card due to the lowest cashback limit of $250/month when compared to the remaining cards. $250/5% = $5k. This means if you spend more than $5k/month already, you will see diminished returns after $5k.

Hopefully, the low cashback cap of $250/month has already discouraged you from choosing this card. If not, the fine print indicating a $4k/month minimum spend before you're eligible for the 5% cashback at Designated Merchants may discourage you. You can only maximize returns with the Smart Card if you spend $4k to 5k/month at those Designated Merchants (e.g. supermarkets).

If you don't spend $4k to $5k/month at the Designated Merchants, this card is not for you.

While the 1.2% cashback on overseas spend seems appealing, there are cards that earn more. Read my post on the Hang Seng travel cards.

- (Cashback) Rate of return - this eliminates the A. Point card which has the lowest rates of return when compared to the remaining Mox cards. This may also eliminate the Smart Card if you don't spend $4k to $5k/month at the Designated Merchants. The 0.56% cashback for General spend is very low when compared to other cards in the table.

If you followed the POE listed above, only the Mox cards are left. In reality, there is only one Mox card. The difference between Mox and Mox+ benefits is whether you have $600k in your Mox bank account to qualify for Mox+.

Other thoughts

- Spend categories vs merchant list - Most people can remember categories (e.g. supermarkets) more easily than specific merchants (Park N Shop). Lists can change, categories less often. Cards with rewards in categories is preferred. Alternatively local vs overseas spend is also easier. It is either/or.

- Rewards based on spending method - High friction. Do I really have to remember and physically do something different when overseas versus local? AlipayHK QR code overseas, but physical card or ApplePay when local in HK to maximize the rewards? I want to ApplePay everywhere or QR code everywhere.

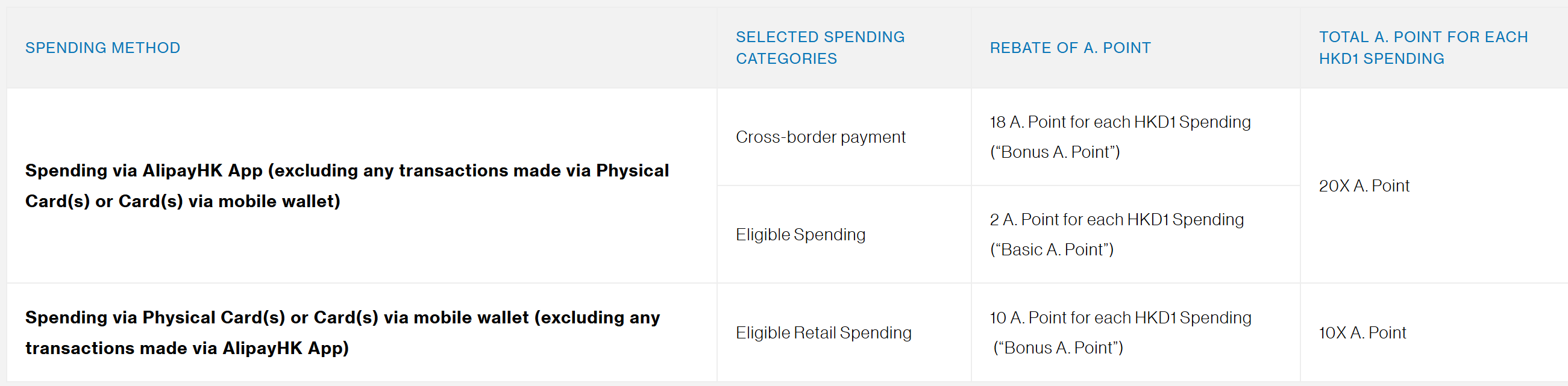

- Transparency - It is already not transparent on Standard Chartered's A. Point card page that 1000 A. points is $1 because the conversion rate is not listed there. You can determine this conversion ratio only if you go into the AlipayHK app and try to redeem A. Points.

Doing the math, you get 20 A. points for $1 spent overseas (only when via the AlipayHK app). While that sounds like 2% cashback, there is a 1.95% foreign transaction fee, so 2% - 1.95% = 0.05% cashback on foreign purchases. Local spending is 10 A. points per $1, so cashback is 1%.

Miles

In addition to the guidance of borrow if you can repay, I'm not a fan of annual fees. Why would I pay an annual fee when I am sometimes not spending money or want to cut down expenses?

Standard Chartered offers 3 mileage cards, and 2 more via its stake in Mox. With the changes to Mox starting July 1st, 2026, the table below lists the options. Amounts are in HKD.

| Card Name | Bank Balance for Annual Fee waiver | Annual Fee (1st year waived) | Foreign Transaction Fee | Overseas Spend |

|---|---|---|---|---|

| Cathay Mastercard - Priority Private (Black card) | $8M | $8K | 1.95% | $2/mile |

| Cathay Mastercard - Priority Banking (Blue card) | $1M | $4K | 1.95% | $3/mile |

| Cathay Mastercard (Green card) | No requirement | $2K | 1.95% | $4/mile |

| Mox+ | $600k | Waived | Waived | $5/mile |

| Mox | <$600k | Waived | Waived | $10/mile |

With Foreign Transaction Fees

I'm not going to cover one-off Cathay welcome offers and other card benefits as there are plenty of other blogs covering the benefits.

The welcome offers have a spend requirement, so going back to borrow if you can repay, I would not encourage you to spend just for the sake of the welcome offer miles. Instead, I will encourage you to incur the least amount of costs while maximizing the return when you do spend money.

If you're only paying Visa or Mastercard exchange rates, either of those are lower than 1.95%, so it is easy to understand a no foreign transaction fee card will naturally be cheaper for most people.

Without Foreign Transaction Fees

Mox are the only cards with no foreign transaction fees. They provide greater financial benefit to you even if the $/mile is higher. This of course means you'll have to spend more money to get the miles needed, but simply doing the financial benefit calculation, the Mox cards win over the Standard Chartered ones.

Do your mileage math

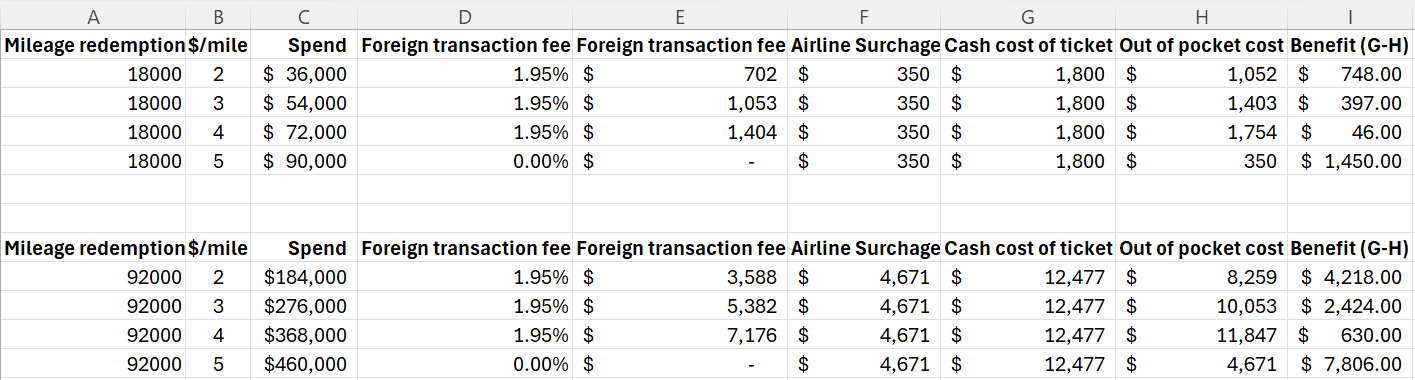

It's pointless to read about best $/mile credit cards without understanding how much benefit you are actually getting in return. Come up with your own calculation on how much you spend to get the miles and how much the cash price is. The results may surprise you.

In my example below, regardless of whether I'm redeeming round-trip flights for 18K or 92K miles, the Mox+ card wins in terms of monetary benefit. If you care about getting the points as quickly as possible to redeem your flight, then only the Cathay Priority Private card (Black card; $8M in the bank account) makes sense.

When the difference in benefits is so great between the Cathay Priority Banking (Blue card; $1M in the bank account) and the Mox+, it does not make sense to me to even consider the Blue card. It's Black card or not at all.

The Cathay Mastercard (Green card) makes zero sense to me when compared to Mox. Even if you have no annual fee, a 1.95% foreign transaction fee + $4/mile cannot be better than $5/mile. For that to be true, 1.95% + $4/mile would have to be equal to $5/mile. $5/mile would thus have to equal 5 x 1.95% = 9.75%. There is a reason you do not see 9.75% cashback credit cards and get offered miles instead. Miles are worth a lot less.

Takeaway

Mox wins for most (cash) benefits and flexibility to switch between cash or mileage over any Standard Chartered card.

While the Cathay cards offer other benefits that may be worth something to you, e.g. lounge, which may make you lean towards the Cathay card(s), if you're like me, tangible cash and predictability is preferred over (lounge) benefits that I may or may not redeem.

It is easily another post to discuss lounge benefits, but I will just leave you with a few thoughts:

- is the food/drink you consumed at the lounge really that much better than what you get onboard the plane?

- would you consume both lounge and plane food? perhaps back to back?

- is there really nothing else you'd rather be doing than parking yourself at the lounge?

Discussion