Stich together your own digital-only bank

Now branded "digital-only" banks, which sounds more trustworthy then "virtual" banks, I'm going to analyze what it takes to build one by examining Mox in Hong Kong.

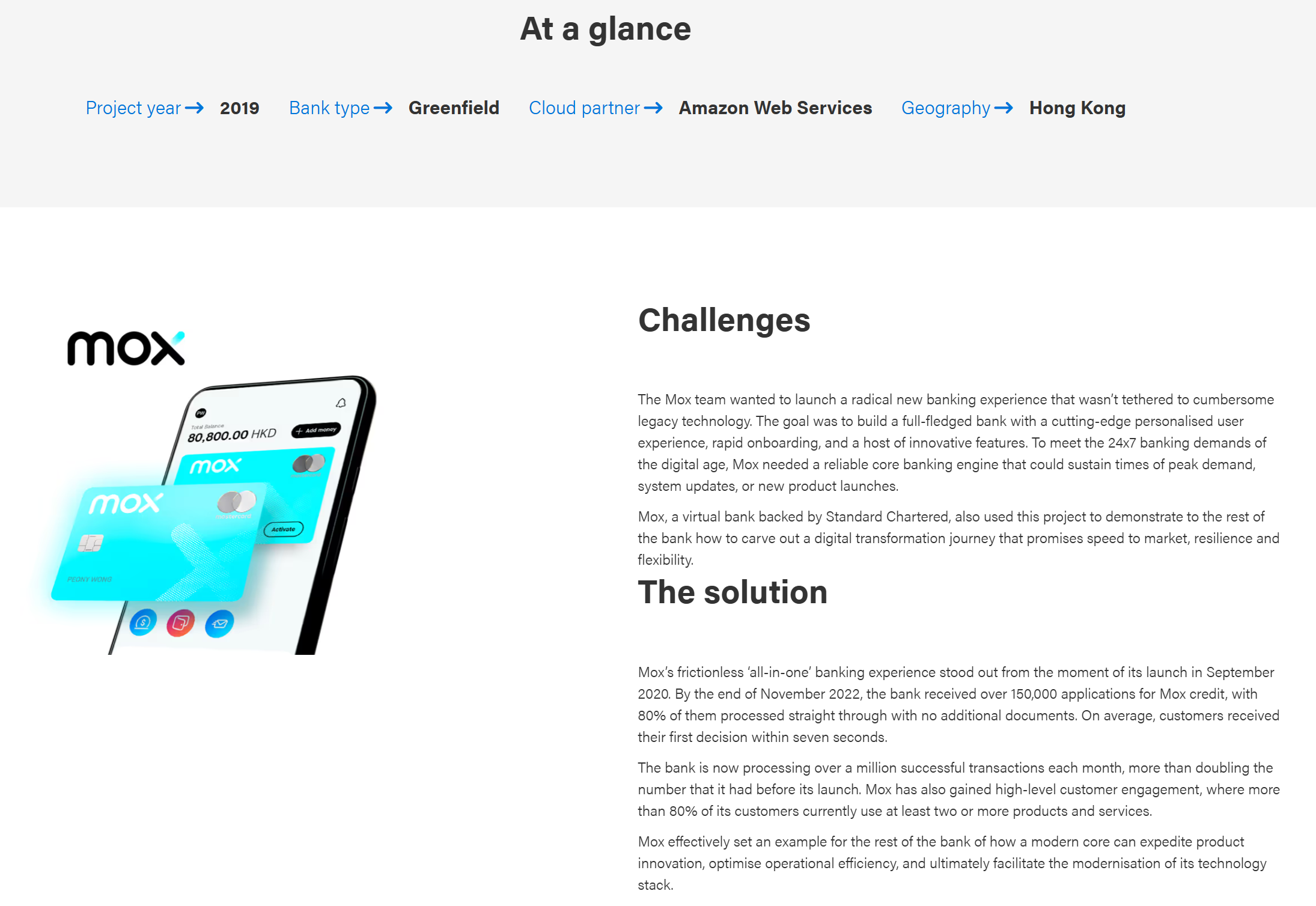

I won't explain all the details of Mox which is a collaboration between Standard Chartered and partners including HKT, PCCW, and Trip.com. It's a smart move to aggregate together common spending categories (banking, telco, travel) to keep customers spending within their ecosystem.

If you go to Mox's website you'll find download links for their app, and I would ask you to please use referral code TJGQ47 to sign up, so both you and I get signup bonuses.

Tech stack details

OK, so how does one build a bank from scratch? It's not easy-easy, but it is easier than the older banks that have been from the pre-internet era of the 1990s.

Here is what I have learned:

- Core Banking Engine: Thought Machine, Vault Core solution

- Cloud providers: Amazon Web Services (AWS)

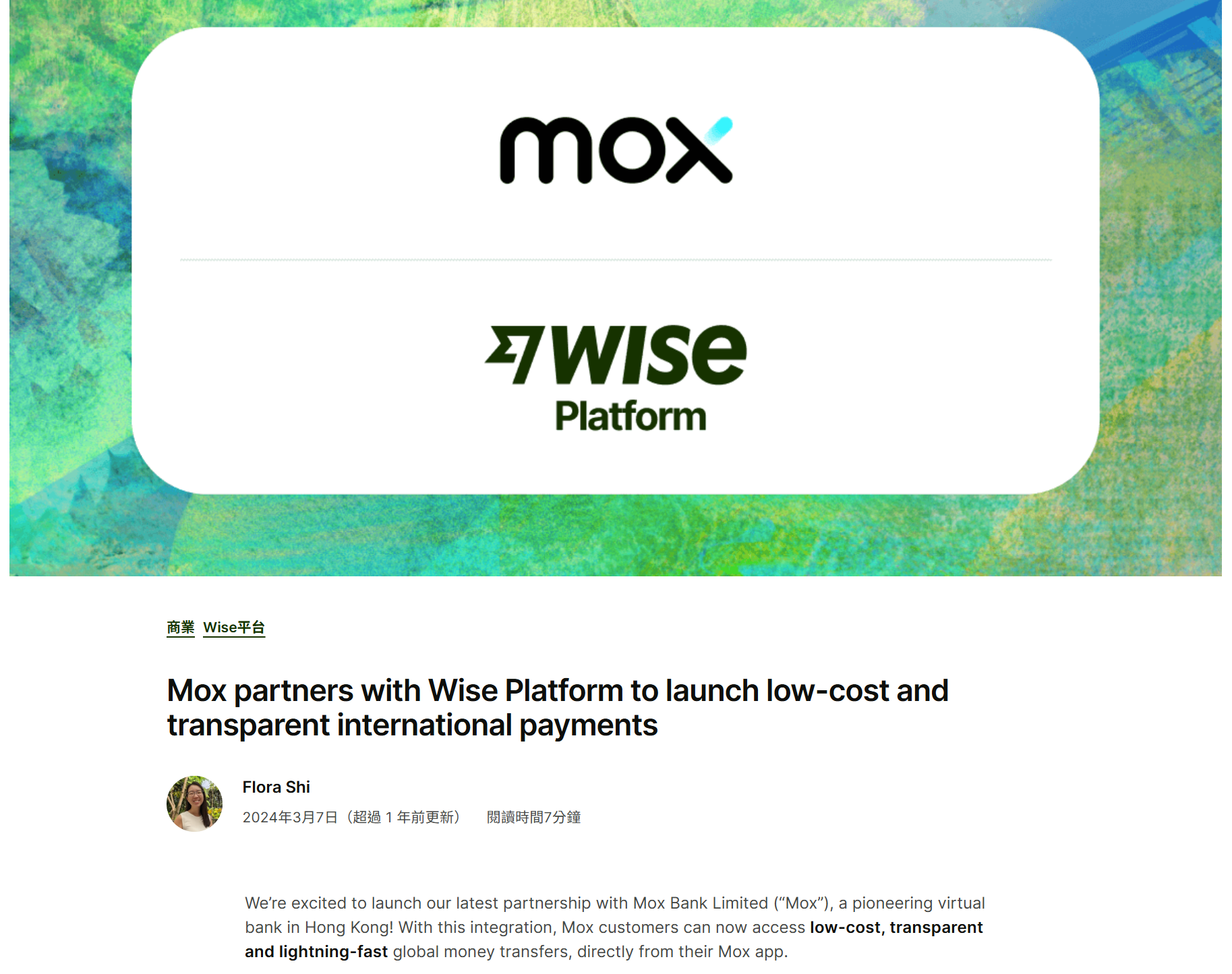

- Global money transfer + foreign exchange (FX): Wise

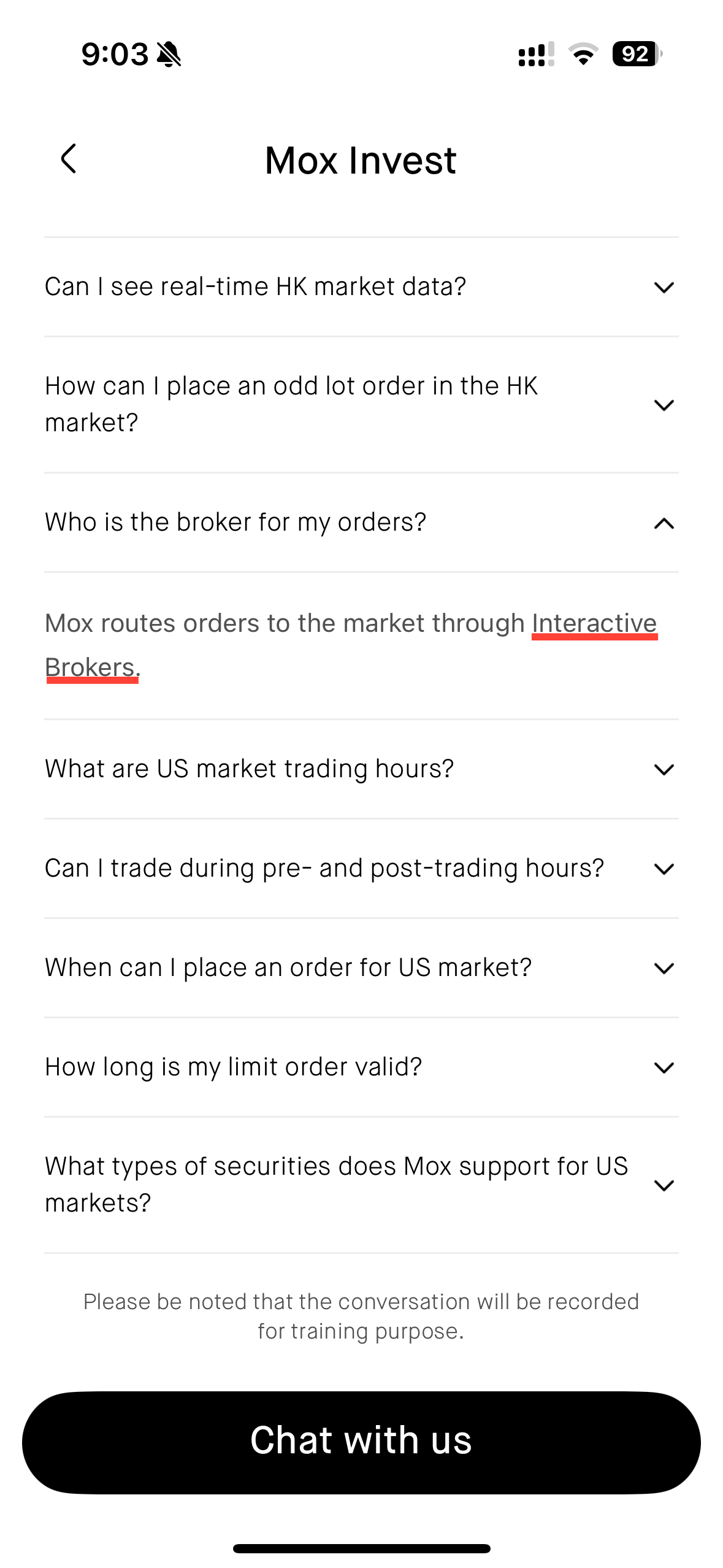

- Stock trading: Interactive Brokers

- Market data: Refinitiv by LSEG, Nasdaq Inc., HKEX Information Services Limited.

- Systems integrator: Vacumnlabs

- Internal engineering: 13 engineers

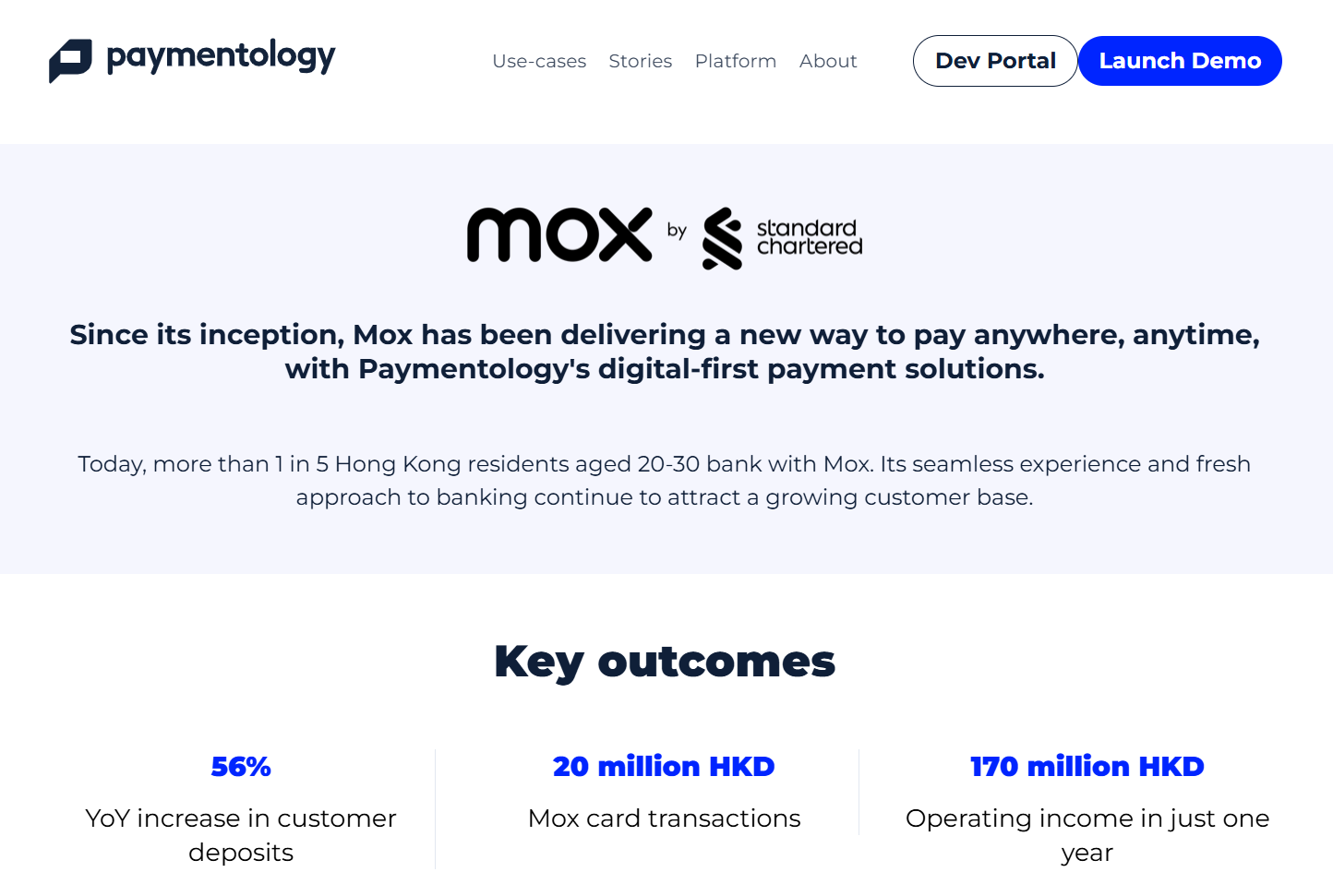

- Payments: Paymentology

- Cards: Paymentology, with 10xbanking and SBS software.

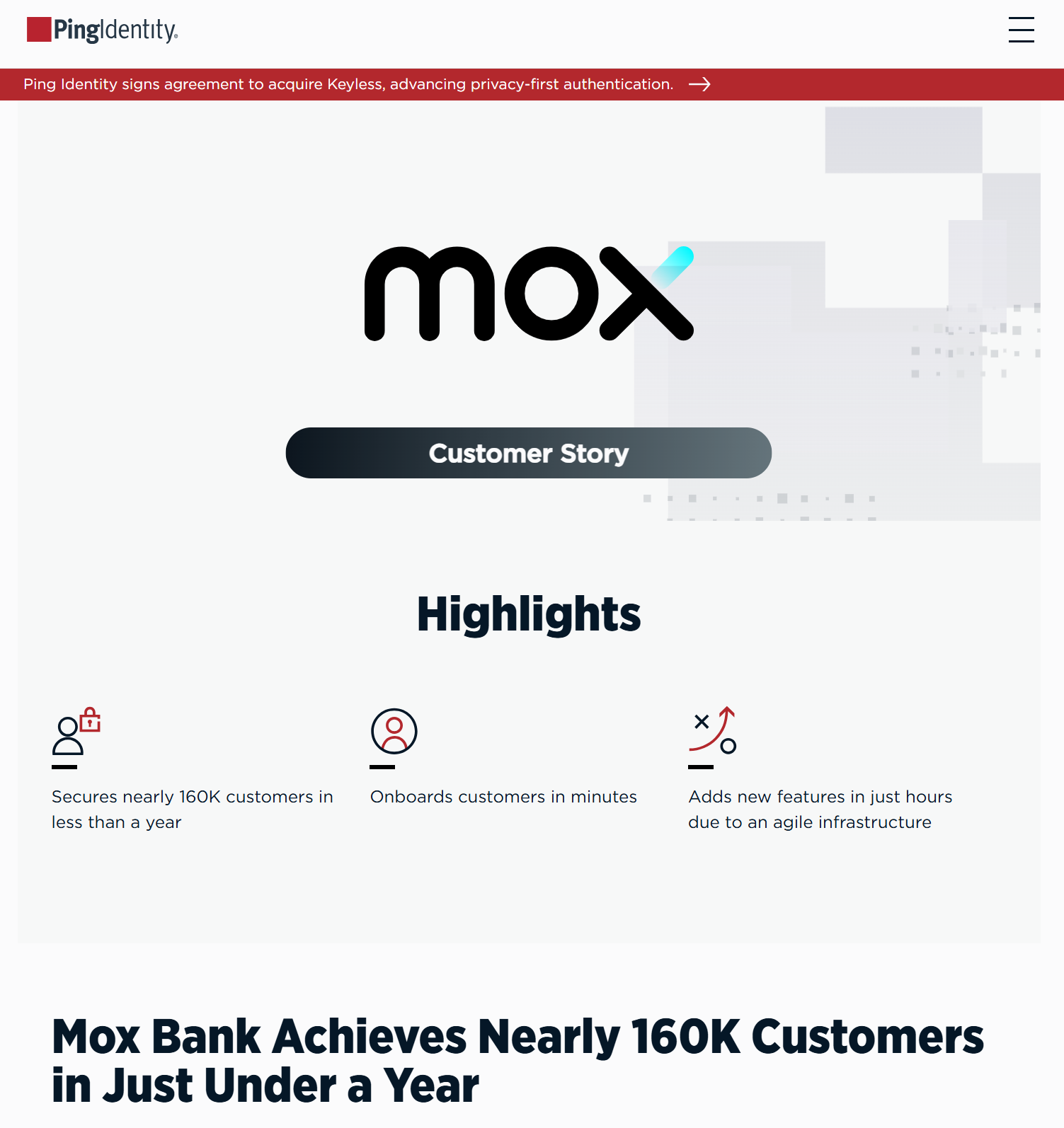

- Identity management: Ping Identity.

- Identity verification: Probably one of the top providers like Jumio. It's been a while since I looked at the signup experience.

- Insurance: QBE Hong Kong

Overall, their timeline is 9-12 months for the initial product launch according to various press releases.

Thoughts on Mox roadmap

It's not a huge leap for Mox to support London Stock Exchange trading support as they already leverage Refinitiv. This will be a product differentiator from other banks which typically offer Hong Kong, China and US stock trading only. It's mostly satisfying LSEG KYC requirements.

If Mox wanted to truly differentiate, I also postulate expanding to even more markets would not be a stretch as Interactive Brokers already offers much broader market reach. Would there be a cost advantage for the customer going through Mox instead of IBKR? Maybe .... but I've always thought convenience is what Mox offers, not necessarily price. Even if it was the same price as IBKR, I'd argue a simple signup for Mox bypassing the redundant KYC for IBKR is still a win for the average trader that doesn't need advanced IBKR tools but just wants broader market access.

Do average traders require more markets? Perhaps not, but that's where you can offer access to more (global) funds to the average trader, or at least a path to that if regulations block less experienced traders to these markets. It's about customer LTV (lifetime value) and not point in time value. As Mox doesn't support stock transfers to/from another broker I think it's most important to get stock trading customers into their system then worry about losing them. The cost of switching is high in the absence of stock transfer support when a customer has to sell their stock, transfer the cash and repurchase the same stock. That can easily result in a few percent loss due to stock price fluctuations and transaction delays.

Before they expand stock trading access though I'd really like them to fix their activity reporting. There's a unique icon for receiving stock dividend payments in the activities history, but a user cannot filter by stock dividend payment activity.

They are adding travel insurance (finally!) which makes a lot of sense, although it competes somewhat with Trip.com's per-trip based insurance offering. Where they can differentiate is annual travel insurance in addition to more comprehensive coverage bundling (e.g. home insurance for theft while you travel, ski injury or hole-in-one golf insurance). That again would increase revenue per customer by keeping the customer spending in their ecosystem, while maintaining low customer acquisition cost and bring sign-up ease for customers.

More advanced spend analysis tools would be useful in making the app even more sticky and encourage user interaction, but I also see a downside of making their customers more aware of what they should or should not use the Mox card for. Generally speaking, the Mox card is great because it is simple for most people: either 2% cash bank or mileage. Advanced credit card owners already use the card selectively to maximize spend for certain categories only.

AWS Details

Thanks for reading if you made it this far. According to this article, Mox uses Amazon Elastic Kubernetes Service, Amazon Managed Streaming for Apache Kafka (EKS, MSK) to fully digitise and orchestrate bank services through Vault application programming interface (APIs).

Knowledge on credit scoring, anti-money laundering (AML) and fraud is sourced from Standard Chartered, its parent bank.

Non-differentiating, but key services for running the bank are operated under the SaaS model to reduce complexity and cost. These include payments, cards, identification and verification (ID&V) and helpdesk.