Best Hong Kong bank for receiving dividends

Mox is the best bank for receiving dividend payments due to its 0.2% dividend collection fee for most people. Signup for MOX using my referral code TJGQ47 and both of us will get more benefits.

You're strongly recommended to learn more at the Investor and Financial Education Council's dividend collection information page first before you read on.

The author of this page has only encountered dividend collection fees for Hong Kong stocks and no scrip fees. Dividend collection fees may differ between stocks listed in HK and other markets. There may also be additional charges or taxes. Do your homework!

For dividend collection fees, let's compare a few other banks in Hong Kong. Banks in HK typically charge the greater of the fee percentage and minimum fee. e.g. if you receive $10K in dividends, a 0.5% dividend fee is $500. The bank will collect $500 instead of a minimum dividend fee of $50.

| Bank | Dividend fee percentage | Minimum fee | Special note |

|---|---|---|---|

| Standard Chartered | 0.5% | $30 | |

| Mox | 0.2% | $30 | |

| HSBC | 0.5% | $30 | Max of $2500 |

| Interactive Brokers | 0% | $0 | |

| Citi Bank | 0.5% | $30 | |

| DBS | 0.5% | $30 | Max of $2500 |

| Dah Sing | 0.5% | $30 | Max of $2000 |

So why did I say Mox is for most people? The math goes like this:

$2500 / 0.2% = $1.25m

This means, unless you have a single dividend payment of $1.25m or greater, a 0.2% dividend fee is less than $2500 in dividend fees that you'll have to pay. Only if you receive a single dividend payment of $1.25m or greater, will you benefit from the max of $2500 in fees. Imagine you have $2m in dividends:

$2m x 0.2% = $10K with Mox, but $2500 (max) with HSBC or DBS.

So why not go with Interactive Brokers which has 0%? Great question. HK has a Deposit Protection Scheme (DPS) of $800K which covers banks. Interactive Brokers is not a bank and not covered. If you're willing to accept the risk of no DPS, then IBRK might be for you.

Is it worth switching to IBRK for zero dividend collection fees?

It depends on your situation. In most cases, I suspect not.

If you're like most people and have accumulated your wealth over time and started with simple stock trading, you probably didn't start with IBRK from day 1 and started trading with one of the banks above. You traded with your bank because account signup was easy. There are either fees to transfer stock you hold with your bank to IBRK, or you take the risk of selling your stock, waiting for the money to settle, transfer it from your bank to IBRK, and repurchase the same (dividend) stock. The stock trading fees and opportunity cost could easily outweigh your dividend fee savings, which means you don't really save anything in terms of dividend collection fees for a few years.

In the less common situation where you somehow didn't trade stock but accumulated a vast amount of wealth, you could bypass opening a stock trading account through your bank and open an IBRK account. You either inherited wealth or started super late in investing I would imagine, so you're also less likely to be overly concerned about dividend fees and/or don't receive more than $1.25m in single dividend payouts.

Who gets $1.25m in dividends?

Very, very, very few people. Less than 5% of the world's population. Imagine you find a stock with an amazing 6% dividend yield.

$1.25m / 6% = $20.83m

I would assume a person has a lot more than $20m, unless that someone concentrated their entire portfolio on one stock. Assuming a person owns at least 4 stocks, that's 4 x $20m = $80m in stocks.

Many stocks have a dividend payout twice per year, quarterly or even monthly. So again, a single $20m dividend is less likely. Assuming twice per year and just one stock out of 4 that pays dividends, that would now be and individual with $100m in stocks: $40m ($20m x 2 in dividends) + $60m (3 other stocks worth $20m with no dividends).

Appendix: Dividend fee screenshots

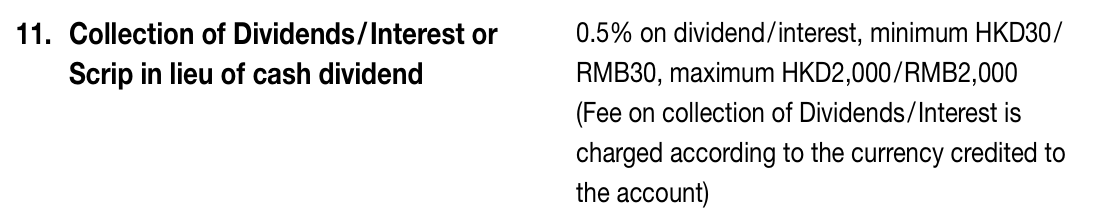

Standard Chartered:

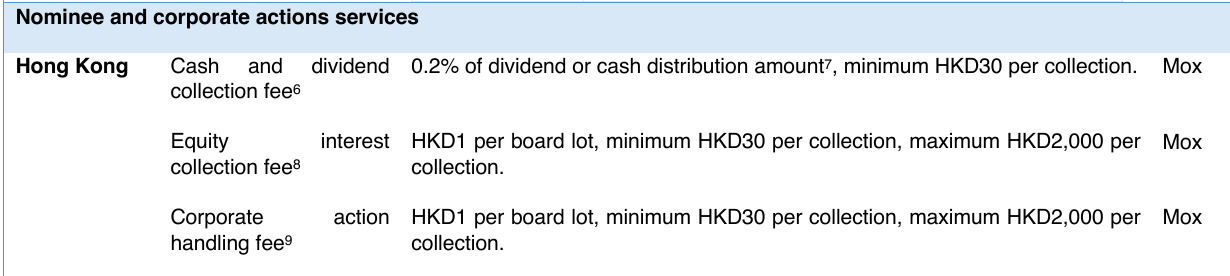

Mox:

HSBC:

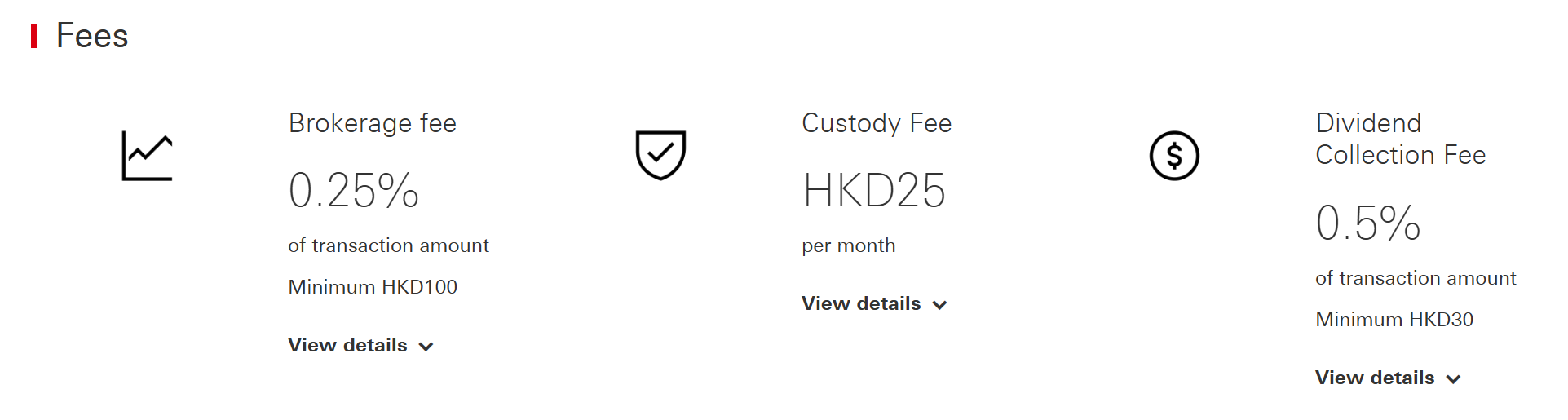

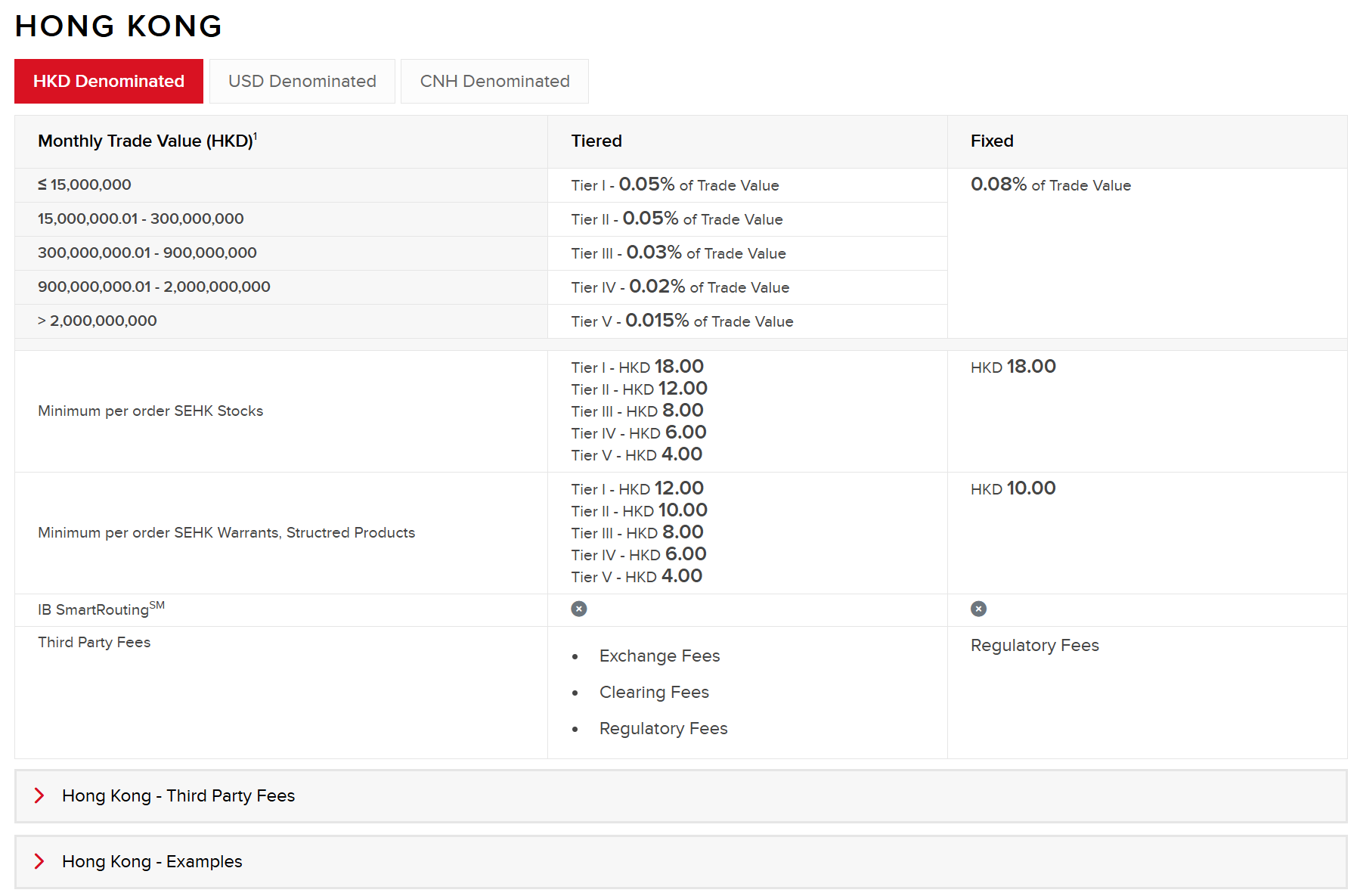

Interactive Brokers:

Citi:

and here's the fine print explaining how corporate actions includes "cash dividends". My feedback is for Citi to make it more transparent. I commend them on attempting the simplify the fees across account tiers, but for some people, burying the details in microscopic text that cannot be easily read without a magnifying glass seems unfair.

DBS:

Dah Sing: